-

REPAY Gateway

-

REPAY Channels

Having trouble? Chat below or contact us.

-

REPAY Elevate

-

REPAY Sigma

-

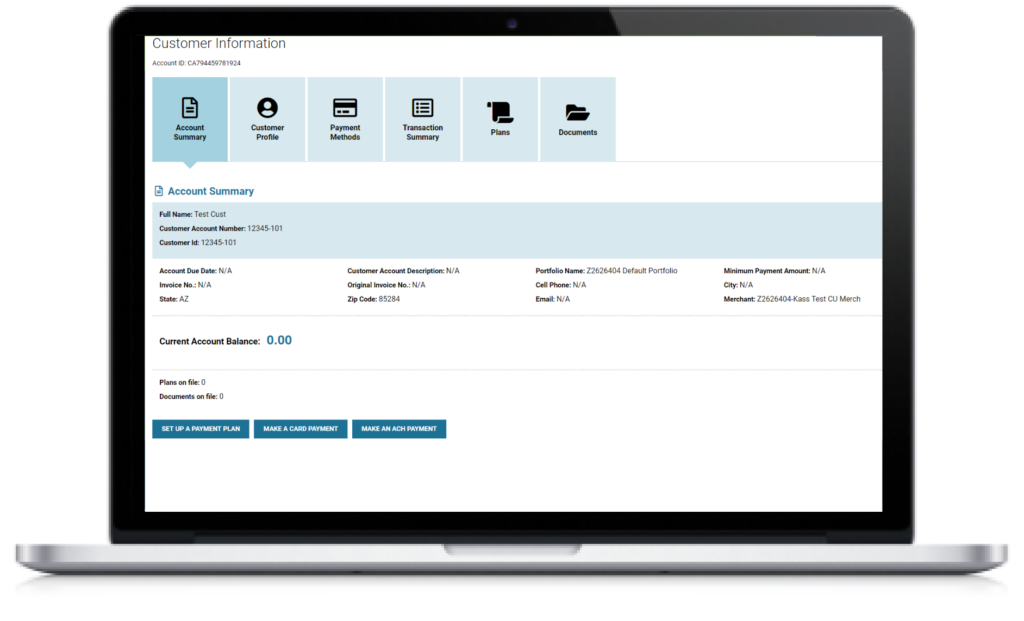

REPAY Paymaxx

-

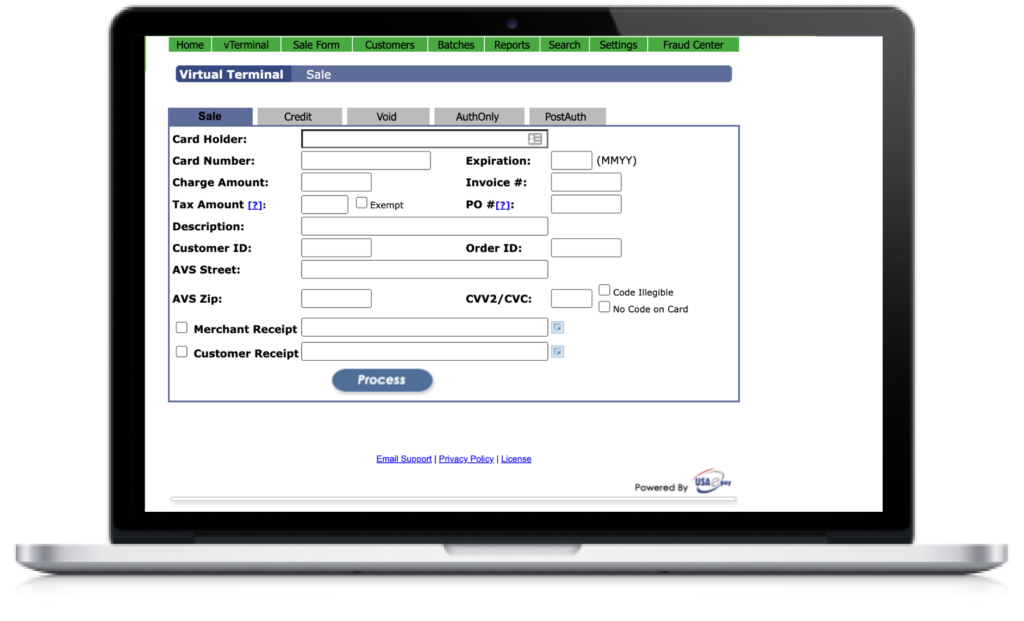

REPAY Legacy Card Gateway

-

REPAY Legacy ACH Gateway

-

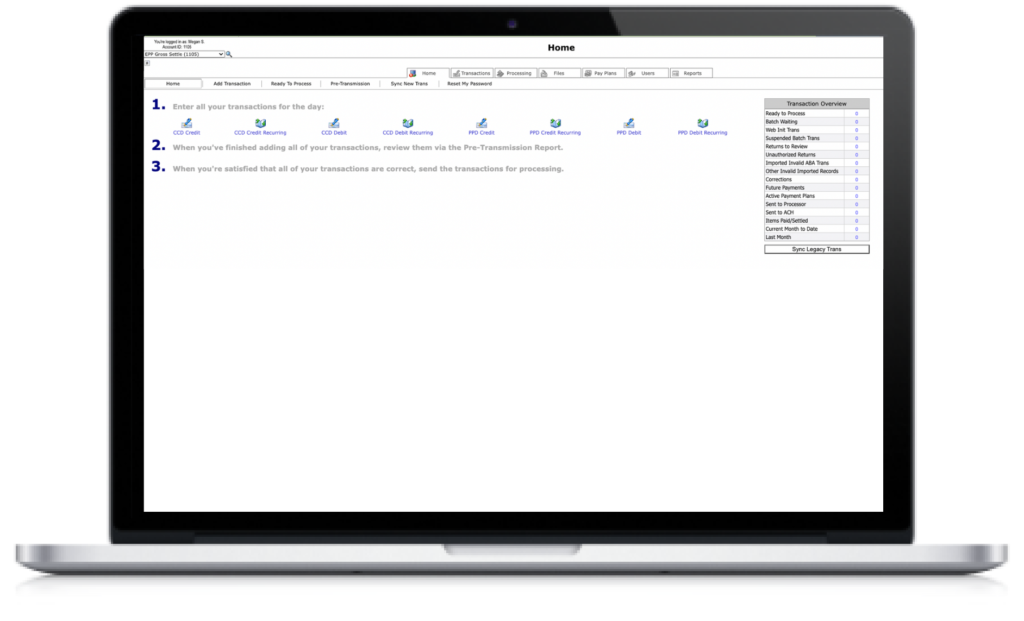

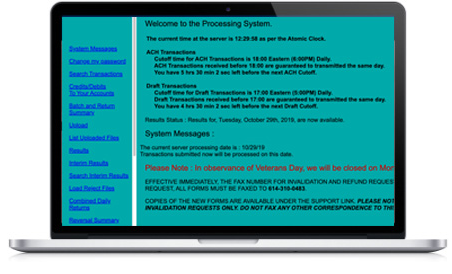

REPAY Legacy ACH Backend

-

REPAY LIFT™ Platform

-

REPAY Vendor Payments (formerly cPayPlus)

-

REPAY B2B Gateway (formerly APSPays)

-

REPAY Payrazr® (formerly BillingTree)

-

REPAY ACHNow (formerly BillingTree)

-

REPAY Legacy Card Gateway (formerly BillingTree)

Partners

-

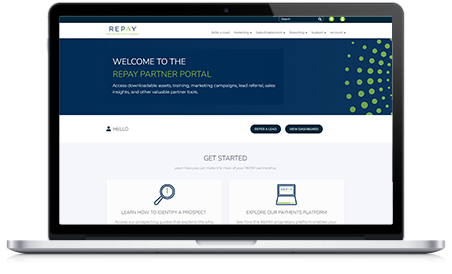

REPAY Partner Portal

-

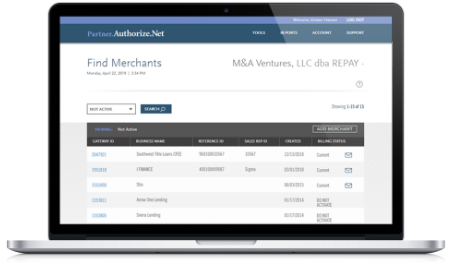

Authorize.net

-

EFT Network

-

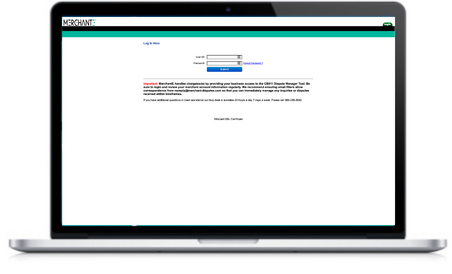

MeS Account Reporting